Real Estate - no bottom

before 2033 and no revival before 2034 !

Stock markets can come down swiftly and loose 50%

in only weeks time. Traditionally, they recover quickly (often in less than 6

months' time). Historically, Real Estate markets need about 75 years to recover.

In some cases, like Florida, they never recover.

Real Estate Cycles

Real Estate cycles are by definition LONG TERM

(+70 year) cycles. Most people will during a life time, only experience one cycle. For this

reason it is extremely important to locate each sub cycle in the Long Term

secular up or down trend. Secular trends last up to 75 years. When

I see the misery the Real Estate market is in and I make a link to the historic

low interest rates, I hold my heart when I realize what will happen once the

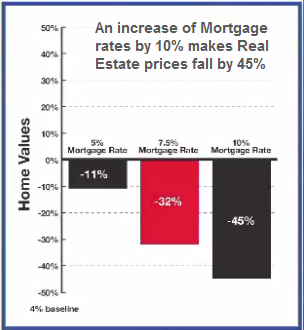

interest rates, under pressure of (hyper)inflation, start to move up .

There is no doubt we have seen the end

of the Secular bull trend and the euphoria of the Bubble we have seen all over

the world will end up in all history books. The actual Secular Bear market trend

for real estate is real and things are getting worse each month.

How low will real estate prices fall?

When you own a house

and your monthly mortgage payment is double the rent your neighbor pays, you

definitely know something is wrong.

I completely disagree with the Talking

Heads shouting that what we see today is nothing more than a insignificant

reaction and that within 3 years from now, Miss Goldilocks will be back holding

the hand of Real Estate. One should understand the potential dramatic

consequences of a Long Term Secular Bear market that has been initiated at a

point where the general level of worldwide INTEREST rates is LOW. Once

interest rates go up (they already do in countries with weaker economies -

and THEY WILL )

under pressure of inflation, the only way for Real Estate is down.

Looking at historical prices

(including Japan), real estate prices, on average, tend to come down by 75 % to

80 % from peak to bottom.

Basically, it is said that after a

parabolic run-up, prices always fall back until on or below the base where the

run initially started from. Conditions in Japan after 1990 and into 1993

are certainly confirming this. Another rule is that Real Estate

prices will come down until the nominal value equals 100 times the monthly rent.

In other words, if the nominal rent is 1,000 $/ € per month, the property's

value will fall back to $/€ 100,000.

This home comes with 4 beds/4baths, two car garage,

installed kitchen, AC and central heating, central vacuum system, nice

garden, up market area...more

A

house steps away from the Ocean?...

Real Estate is a

High Order Capital Good and will be adversely affected by the economic

depression, the over-supply, higher interest rates, lower real income and aging

Baby boomers...but any crisis also offers opportunities and opportunities we

have if we can buy NEW Homes at half the price it would cost to built them

today......AND Real Estate is better than Fiat Paper Money and Treasuries.

Buy a condo in sunny Florida for € 50,000 or

a Single Family home for € 149,000 !

A Real

Estate cycle last 76 years. Real Estate is a High Order Capital good and

the price level of

these goods always fall during a hyperinflationary

depression. Interesting

is that the Real Estate bubble started to deflate in the USA first

and that the action was followed in sequence by those countries where

there was no or little War damage: England, Ireland, Spain, Portugal and

Greece. So far the countries which were actively involved in the 1st and

the 2nd World War like The Netherlands, Germany, Belgium and France, the

Real Estate sector has only recently come to a standstill and the market

has dried up but no real crash has been experienced yet. In Greece however

Real Estate prices started to crash severely as soon as the local Bond

market collapsed. Similar scenario's can be expected for Italy, Portugal

and as soon as 2012 also for France and Belgium.

Real Estate prices have been

thriving on artificially low interest rates making Mortgages cheap.

Because of debt being too cheap, consumption is abnormally

stimulated and savers are abnormally punished. Real savings (capital)

which are the life line for society is destroyed and chased away.

As the economy deteriorates the

Authorities increase the taxation and because Real Estate cannot be moved

around it becomes the main tax target: capital gain tax and wealth

tax are applied (if not applied by the local government it is enforced by

the IMF and ECB).

move mouse over chart for alternate

figure

Increased

taxation and expensive hard to get mortgages adds pressure on a market which is

already suffering from lower demand as a result of lower Real Income and higher

supply as a result of the Real Estate bubble and the retiring Baby boom

generation..

During the Weimar hyperinflation one

month's rent barely paid for one loaf of bread. Many tend to forget that

Real Estate (especially a home) wears out, gets old, is badly isolated,...During

recessions and depressions Authorities do all they can to keep rents as low as

possible (housing is part of the inflation indexes) and as a rule block rents

during hyperinflation. As a result Landlords see their income and right

amputated, the income on their property disappear and try to sell.

Posted August 1, 2011

My parents bought a small three-bedroom house in Texas in

1960 for the seven of us in the family. My brother and I shared one bedroom, my

parents had the center bedroom and my three sisters shared the back bedroom. The

house cost about $12,000. Today it’s probably worth $120,000. My parents put

down about 15%, that’s all they could afford on a 15-year mortgage.

They didn’t look at it as an investment. At best they may

have considered it a sort of savings plan. Owning a house was viewed as an

expense just like operating a car. You might need shelter but painting and small

repairs were constant. If someone had gone to them and suggested it was a great

investment because housing could only go up, they would have looked at him like

a goat with three heads. Housing an investment? Are you kidding? At best you

might break even and it would take 18 months to sell.

Posted January 20, 2011 -

Home price drop in the USA exceeds the Great

Depression.

Home prices have fallen 26 percent since

their peak in 2006, exceeding the 25.9 percent drop registered in the five

years between 1928 and 1933, the housing data company said in a report on

Monday. Prices fell 0.8 percent over the month...more

Updated December 2010 [November 27, 2009] - This is the REAL PRICE evolution of Real

Estate...

US Home price expressed in Real Money

US Gold price - Gold ratio

Updated July 6, 2010 - The main difference between Real Estate and Stocks

is that it usually takes a generation before real estate losses are recovered.

Stock market losses occur more frequently, can be severe (-50% in 2008), but

recovery of all losses often happen in less than a year time.

Previous Tops & Bottoms in Real Estate:

Top

Bottom

Top

Bottom

Top

Bottom

Top

Bottom

1772

1799

1851

1877

1928

1955

2006-07

2033

Whatever is written and said all over the world,

we expect Real Estate prices to continue to slide

down

in 2010 and 2011. A small correction is however possible in 2012 but then

the slide will resume until 2033. Real Estate is a High Order Capital good

and it will be definition be affected by the recession and depression.

"A young couple with excellent

credit and a solid income who bought an average three-bedroom house for $

585,000 in 2006 is paying $ 4,300 per month. Because of the bursting Real

Estate bubble, their house is now worth only $ 187,000 - though they till

own $ 560,000 on their mortgage. Just to recover the equity will take 60

years!

Underwater homeowners can either

continue to pay $ 4,300 a month. Or they could go into foreclosure, rent a

place for $ 1,000 a month, and in a few years buy a home at a pre-bubble

price of $ 180,000 with monthly payments of $ 1,200."

Posted November 2010

How to dig a financial hole of $/€ 600,000!? Amazing is that

many Europeans refuse to LEARN from what happened in the USA and Spain

and still BELIEVE what the Authorities say...In

2005 RIGHT BEFORE the American Real Estate busted, Bernanke himself

testified that there was no Real Estate Bubble and that it was safe to

buy property. In 2006 the bubble busted and today somebody who bought a

house in 2006 at $ 500,000 and made a $ 100,000 down payment has a

debt of $ 800,000 (capital plus interest). His house however is worth

ONLY $ 200,000. The end result is that instead of being better off

by buying a property, those people digged a financial hole of $ 600,000

! Those who have the guts to watch the clip to the end will understand

what we are talking about...

September 23, 2009

A landmark ruling in a recent Kansas Supreme Court case

may have given millions of distressed homeowners the legal wedge they need to

avoid foreclosure. In

Landmark National Bank v. Kesler, 2009 Kan. LEXIS

834, the Kansas Supreme Court held that a nominee company called MERS has no

right or standing to bring an action for foreclosure. MERS is an acronym for

Mortgage Electronic Registration Systems, a private company that registers

mortgages electronically and tracks changes in ownership. The significance of

the holding is that if MERS has no standing to foreclose, then nobody has

standing to foreclose – on

60 million mortgages. That is the number of

American mortgages currently reported to be held by MERS. Over half of all new

U.S. residential mortgage loans are registered with MERS and recorded in its

name. Holdings of the Kansas Supreme Court are not binding on the rest of the

country, but they are dicta of which other courts take note; and the reasoning

behind the decision is sound...click

here for more...

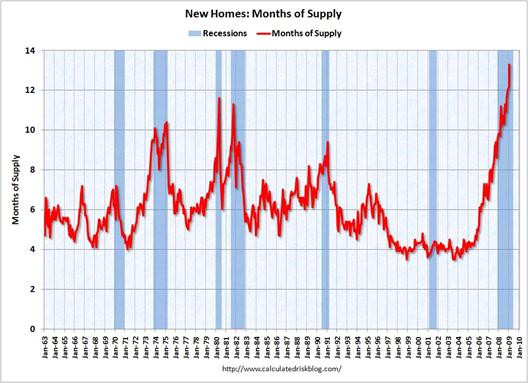

May 22, 2009 - With this huge supply of new homes,

there is no room for improvement

May 1st, 2009 - Danger as we move out of the Eye of the storm

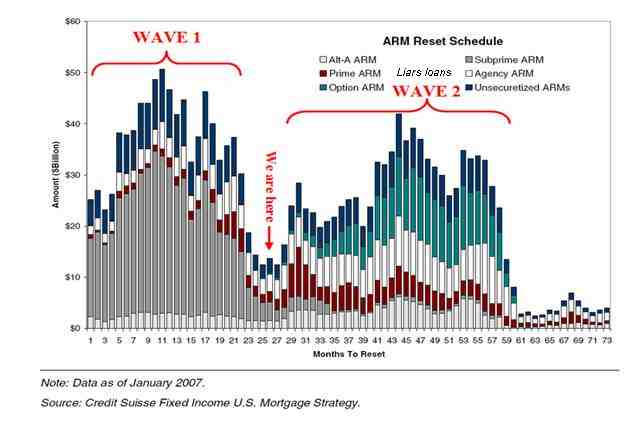

into the 2nd Wave!

More bad news for Real Estate.

The number of foreclosures in the US keeps going up. What people are looking at

is the schedule of mortgage resets for option ARM loans [also called liar

loans]. These will begin to reset in a couple of months and the process will not

peak before 2011.

April 22, 2009 : in the USA 600,000 foreclosed houses

are kept off the market by the lenders.

“’We believe there are in the

neighborhood of 600,000 properties nationwide that banks have repossessed but

not put on the market,’ said Rick Sharga, vice president of RealtyTrac, which

compiles nationwide statistics on foreclosures. ‘California probably represents

80,000 of those homes. It could be disastrous if the banks suddenly flooded the

market with those distressed properties. You’d have further depreciation and

carnage.’

According to the Wall Street

Journal: “Ronald Temple, co-director of research at Lazard Asset Management,

expects home prices to fall 22% to 27% from their January levels. More

than 2.1 million homes will be lost this year because borrowers can’t meet their

loan payments, up from about 1.7 million in 2008.” (Ruth Simon, “The housing

crisis is about to take center stage once again,” Wall Street Journal)

A similar pattern is used

by Spanish banks. (Spanish banks over invested in Real Estate as they were

sure trees would grow all the way into heaven)

April 17, 2009 - the next shoe to drop is Commercial

Real Estate -

Updated March 31, 2009

This is a very

interesting long term chart of Real Estate. To see just how unusual recent price

activity has been, take a look at Yale economist Robert Shiller's

inflation-adjusted housing chart, going back more than a century.

The chart makes it crystal clear that the current

overvaluation of real estate in real terms grossly exceeds the one during the

1920s. The coming correction in real estate will be protracted and

gut-wrenching, with an expected cumulative effect that is much worse than the

Great Depression.

Posted March 31, 2009

The Real Estate Boom was nothing more than a desert

mirage. The direct result of fractional reserve banking and the creation of

money out of thin air.

The Real Estate crisis and the freefall of home prices

is expanding to commercial properties.

Other countries like the UK, Spain, France, Belgium, Morocco, Canada,

Costa Rica, Belize, Austria and East European countries have joined the

USA as their real estate bubbles also are deflating.

Trees nor Real Estate grow all the way into Heaven!

I understand that for many it is extremely hard

to understand what is happening right now as a Real Estate cycle is in most

cases a 'once in a lifetime experience' and they saw nothing else than rising

prices (apart from some short term corrections). Even the Paradise

of Real estate: the city of London, Manhattan and the paradise resorts in the

Gulf petro-monarchies are becoming a real estate hell.

The real estate crisis has become a self feeding

monster. The Real Estate crisis

is amplified because banks keep reducing the number of mortgages and real estate

loans to potential buyers.

As a rule of thumb, in a secular

real estate bear market Real Estate prices fall until the price equals 100 times

the rent.

Another rule is that a Home should cost no more than three times annual

household income.

Purchasing a house creates dead capital. It does not

create jobs once the construction is terminated, but consumes capital through

the financing.

The wealth created by Real Estate is mainly an

illusion created by currency movements. (South Africans bought

automobiles, drove them a couple of years and sold them at a profit because the

Rand used to be so weak).

The harder it gets to borrow money to buy a home, the

harder Real Estate prices will fall.

Best case scenario, the Debt crisis and the US-Real Estate

won't bottom until 2011 and probably 2017. For the EU and other countries, as

the crisis started with a delay, expect to see the bottom with the same delay.

For the EU this could well be 2014-2020.

When the Argentinean Real Estate sector bottomed it

had become impossible to get a mortgage to buy property (it still is).

Real Estate is a LEVERAGED good. Hence it's general

price level is directly affected by the level of interest rates.

Monetary inflation is even more deceptive - or

dangerous - when it is working with asset deflation.

What happens when monetary inflation meets asset

deflation is not understood by most of the population. Hidden within the

convergence of those two fundamental forces will be the likely "solution" to the

current housing crisis, as well as opportunities for astute individuals to

protect and even increase their net worth during a time of falling real home

prices."

Posted January 9, 2009

When I discussed the imminent crash of the

Japanese Real Estate and Stock market in 1989, experts said

I was crazy. Japan was an overpopulated island and for this

reason alone a Real Estate crash would and could never occur. And yet, 15 years

later, a house selling for 220,000 yen in 1989 can be bought for 80,000 yen. Not

only has Japanese real estate crashed, but the Yen has also...a terrible shock

for all 1989 non-believers. Today similar conditions occur for British real

estate owners: on top of sliding British real estate prices, the Pound is also

crashing.

People are so naive to believe that what happened

in Japan would never occur in the United States, Australia, the City of London,

the Costa del Sol in Spain or Belgium...and yet it is happening in all of these

countries!

Stock markets can come down swiftly and loose 50%

in only weeks time. Traditionally, they recover quickly (often in less than 6

months' time). Historically, Real Estate markets need about 75 years to recover.

In some cases, like Florida, they never recover.

Posted December 22, 2008

December 2008, the commercial Real Estate

bubble is - as expected - bursting. In November analysts at Credit Suisse

said two big commercial mortgages that had been packaged into securities in the

past year were likely to default. The rapid deterioration of these loans fed

worries that the weakening economy and higher unemployment rate would drag down

the $800 billion market for commercial-mortgage-backed securities,

or CMBS, which so far has withstood the credit crisis with low delinquency

rates.

Updated March 17, 2009

"You don't get rich by buying a house! You get rich by investing your

money wisely. By buying a house in today's market, you could even get

poor!"

"What asset or Real Estate deflation

(in inflation-adjusted terms) and monetary inflation have in common is that they

are complementary (not opposing) forces of financial destruction. Asset

deflation destroys the purchasing power of your assets even as monetary

inflation destroys the purchasing power of your money".

Today one can buy Real Estate

below $ 10,000. Some of these opportunities are wise investments! The housing market for the next

several years will undoubtedly take a severe hit. In the end the torrential

flood of homes that come to market for sale will be bought at much lower prices

by my children as well as yours at prices which are affordable. Those who count

on 'a dip' in the market will be amazed how deep the Real Estate market can

slip!

Posted July 23, 2008

Only $ 5,000 for a three-bedroom house! This is a foretaste of what Spanish

builders may expect in the near future.

July 23 (Bloomberg) --

Fannie Mae, the largest U.S. mortgage finance company, couldn't find a

buyer who would pay $6,900 for the three-bedroom house at 1916 Prospect

St. in Flint, Michigan. So broker Raymond Megie, who is handling the

foreclosure sale, advised cutting the price to $5,000.

Megie still couldn't sell it. ``There's

oversupply,'' he said. The home sold in 2005 for $110,000.

Click here for more...

There are also

some people out there -- and I know at least one of them -- who decided

not to put their money in the stock market but rather base their

retirement portfolio on rental properties, typically a very safe and

responsible that. Nonetheless, the recession has now gotten so bad that

even these types of investors are suffering.

Anecdotally,

the story I heard from one poor soul is that three of four of his rental

tenants are least three months in arrears on their rent, and this has

put him in arrears on his mortgage payments. It would be a tragedy for

someone like this to wind up in bankruptcy and without retirement money

because of the ripple effects of this recession.